![[Valid Atom 1.0]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_tCMK2LqihiqzbpwXuba1Ad1TFw3FG0Tsma3v20pGNqtLCE70Mf54_DQNPmrQ_h-iHMDr6zwijxVhG2bT7gRtr40RVYgrLEo25fSLSYIQ9dJko=s0-d "Validate my Atom 1.0 feed")

Guide to Put-Call Ratio

What is Put/Call Ratio?

Put/Call ratio (PCR) is a popular derivative indicator, specifically

designed to help traders gauge the overall sentiment(mood) of the

market. The ratio is calculated either on the basis of options trading

volumes or on the basis of the open interest for a particular period.

If the ratio is more than 1, it means that more puts have been traded

during the day and if it is less than 1 it means more calls have been

traded. The PCR can be calculated for the option segment as a whole

which includes individual stocks as well as indices.

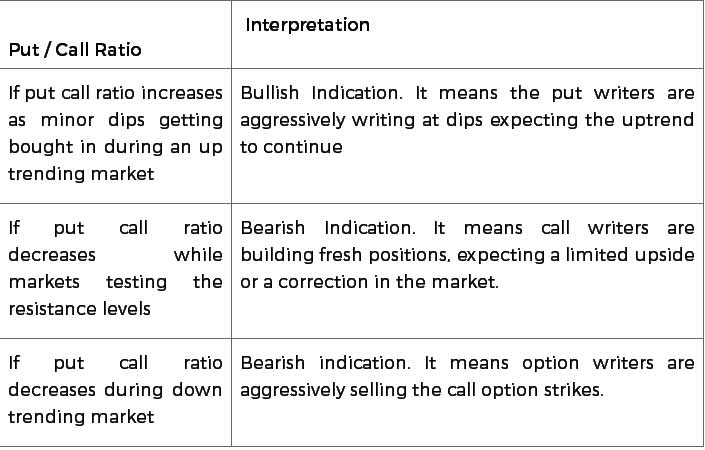

How to Interpret Put/Call ratio

The Put/Call ratio is mainly used as a contrarian indicator. Markets in

the short-term are driven more by the emotions than fundamentals.

Times of greed and fear in the market are reflected by significantly

high or low PCR. Contrarians say, PCR is usually headed in the wrong

direction. In an oversold market, puts will be high; as everyone

expects the market to fall more. But for contrarian trader, it suggests

that the market may soon bottom out. Conversely, in an overbought

market, the number of calls traded will be high expecting the market to

trend higher but for contrarians, it would suggest that market top is

in the making.

There is no fixed range that indicates that the market has created a bottom or a top, but generally traders will anticipate this by looking for spikes in the ratio or for when the ratio reaches levels that are outside of the normal trading range.

If options were held only to make directional bets, this analysis would have held true, however traders trade options for reasons other than making directional bet. Traders could buy options to hedge their existing position as well as to create income generation strategies. So with a combination of speculation and hedging activities, relying solely in terms of higher or lower number of Put Call ratio may not be fruitful.

Let’s see how vague PCR can be, if used in isolation.

There is no fixed range that indicates that the market has created a bottom or a top, but generally traders will anticipate this by looking for spikes in the ratio or for when the ratio reaches levels that are outside of the normal trading range.

If options were held only to make directional bets, this analysis would have held true, however traders trade options for reasons other than making directional bet. Traders could buy options to hedge their existing position as well as to create income generation strategies. So with a combination of speculation and hedging activities, relying solely in terms of higher or lower number of Put Call ratio may not be fruitful.

Let’s see how vague PCR can be, if used in isolation.

Bank Nifty futures vis-à-vis Bank Nifty PCR

In the above example of Bank Nifty, we had witnessed a steady increase

in PCR from May 2016 to 15th July 2016. Con-currently we saw a rise in

price of Bank Nifty as well. In Dec 2016 Bank Nifty resumed its fresh

uptrend but PCR fell sharply. This contradicts with the relations

experienced earlier. From May 2017 till July 2017, PCR has once again

moved in tandem with Bank Nifty. PCR as an indicator on its own has

flaws. PCR levels in a highly volatile market can be misleading as

typically, during such times; traders tend to sell puts instead of

buying calls. So, analyzing put call ratio based only on high or low

PCR numbers could prove costly. Thus it is important to use Put Call

ratio in sync with other trading activities.

PCR Analysis

Let’s see how PCR analysis can be interpreted taking option sellers

into consideration who are the major players in the market as compared

to the retail public who are usually on the buying side of the trade.

Traders can combine options data including the Put Call ratio with

implied volatility to gauge if long or short positions have been

created in the market.

Traders can combine options data including the Put Call ratio with

implied volatility to gauge if long or short positions have been

created in the market.

1) Build-up in options along with increase in IV’s (Implied Volatility) suggests long formation

2) Build-up in options along with fall in IV’s (Implied Volatility) suggests short formation

Types of View based on Open Interest, Implied Volatility and Put Call Ratio:

Chart A –Nifty Futures July Series

(Upper Sub Graph –Nifty Futures Price, Green Line –Nifty Futures Open Interest)

Chart B- Nifty 10,000 July CE

(Upper Sub Graph-Nifty 10,000CE, Blue Line –PCR, Red Line-Implied Volatility 10,000CE, Green Line –Open Interest 10,000CE)

Chart A: Nifty futures witnessed a swift increase in prices from 9650 levels to 9950 levels where the markets started to consolidate, coinciding with a gradual increase in Nifty futures O.I. Traders at this levels started to create fresh short position in the futures market, expecting the market to correct as the open interest surged higher along with a small drop in prices.

Simultaneously in Chart B from 10th July to 20th July we witnessed call writing in OTM call option strikes including 10,000CE(as shown in the above graph) as the traders expected market to correct or remain range bound and not cross 10,000 levels in the current series. This is indicated by a decrease in PCR and increase in Open interest of Nifty OTM call options including 10,000CE strike during the same timeframe.

As price of Nifty futures started to increase from 23rd July, traders who were short in the futures market along with the call option writers had to run for a cover and close their short positions. This panic was observed by a sharp decline in the open interest positions of Nifty future contracts. In addition, implied volatility also tumbled along with an increase in Put Call ratio due to unwinding of open positions in short call option strikes.

Any smart trader, by analyzing the above mentioned positions in Nifty futures and call options could have taken a bullish stance by anticipating a huge short covering in the markets.

Chart A: Nifty futures witnessed a swift increase in prices from 9650 levels to 9950 levels where the markets started to consolidate, coinciding with a gradual increase in Nifty futures O.I. Traders at this levels started to create fresh short position in the futures market, expecting the market to correct as the open interest surged higher along with a small drop in prices.

Simultaneously in Chart B from 10th July to 20th July we witnessed call writing in OTM call option strikes including 10,000CE(as shown in the above graph) as the traders expected market to correct or remain range bound and not cross 10,000 levels in the current series. This is indicated by a decrease in PCR and increase in Open interest of Nifty OTM call options including 10,000CE strike during the same timeframe.

As price of Nifty futures started to increase from 23rd July, traders who were short in the futures market along with the call option writers had to run for a cover and close their short positions. This panic was observed by a sharp decline in the open interest positions of Nifty future contracts. In addition, implied volatility also tumbled along with an increase in Put Call ratio due to unwinding of open positions in short call option strikes.

Any smart trader, by analyzing the above mentioned positions in Nifty futures and call options could have taken a bullish stance by anticipating a huge short covering in the markets.

-----------------------------------------------------------------------------------------------------------

↪Disclaimer:

Before using this post, please make sure that you note the following important notice. Information provided in this post for the educational & informational purpose only. Visitors/Viewer/ followers are advised, before making any investment decision from this post, you should do independent research. The use of this post or information for your own benefit is at your own risk.